We gather some interesting data here at DG Cities. For this short blog, we thought it would be useful to share insights from our research into the factors influencing electric vehicle take-up across the UK. Here, our Head of Delivery, Balazs Csuvar explains some of the numbers and the value of a local authority’s EV strategy in supporting the transition…

While the sector is growing rapidly, overall take up of electric vehicles in the UK is still quite low. In this blog, we wanted to explore where EVs have been picked up, the factors influencing uptake and how quickly they will become the dominant vehicle type across the UK.

Of all registered vehicles in the UK today, ~1.9% are electric or plug-in hybrid. These ~750,000 vehicles are not equally distributed across the country, with the majority of local authorities having less than 1% EVs. By comparison, in Norway, 16.9% of all vehicles are electric (23% including plug-in hybrids).

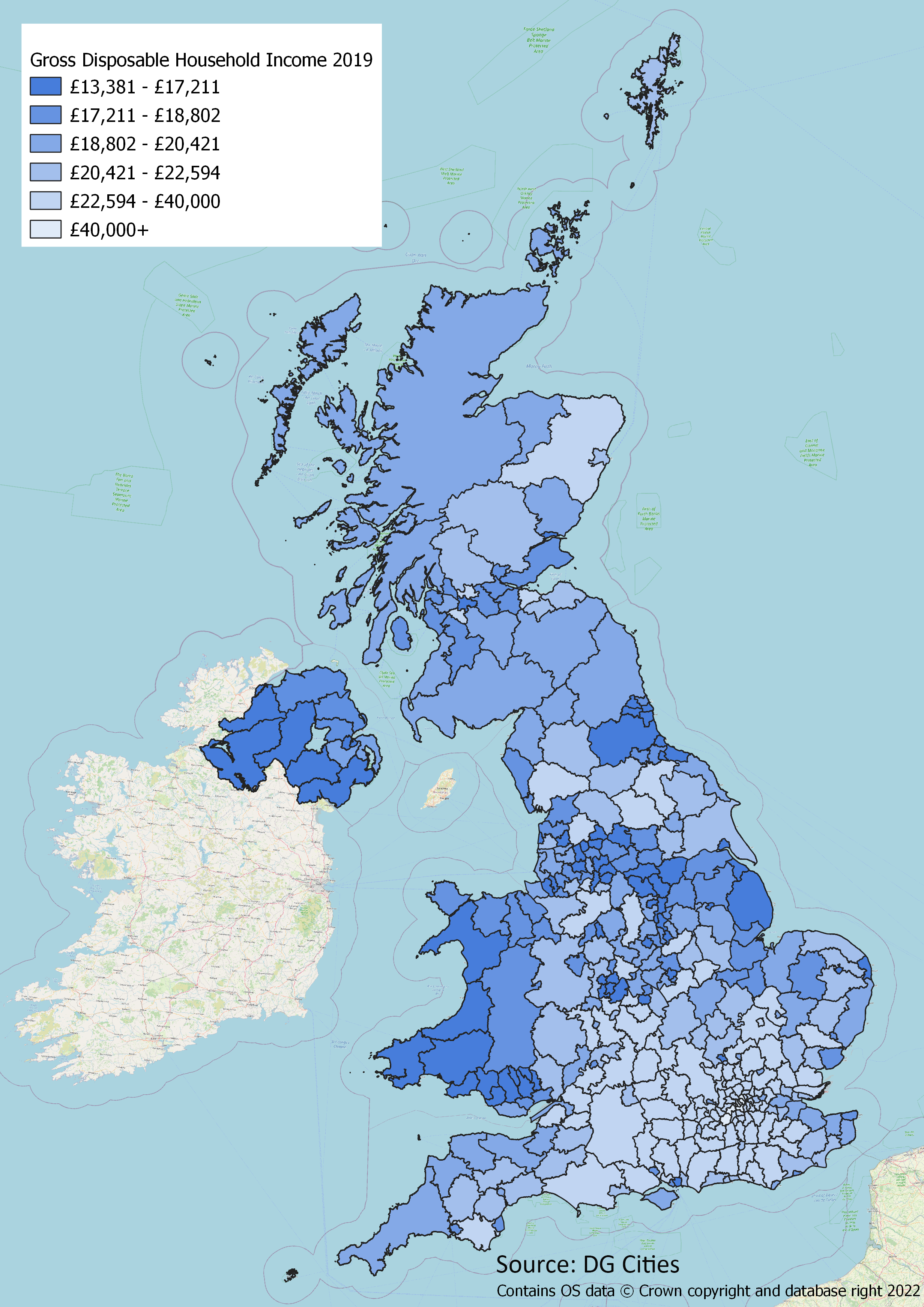

Early EV adoption has tended to occur in wealthier areas. Disposable household income is an important factor in defining where electric vehicles have been purchased - data shows a clear correlation between GDHI (gross disposable household income) and EV uptake, as seen in the chart below.

Income, however, is not the only factor. Available EV charging infrastructure also plays a huge role in supporting the transition, with a clear correlation between EV uptake and available charging points per person. The availability of infrastructure helps to build confidence. The data and our experience shows that local authorities can get ahead and help people make the switch to EVs by creating a reliable and accessible charging infrastructure for their residents, visitors and businesses.

This chart below illustrates whether or not councils have an EV strategy. It’s not surprising to see that the majority of local authorities with a large number of charging points do have a strategy, either at a county or local level. As the data shows, developing a strategy to support the transition is possibly the best way to kickstart any council activities in this field.

How can we expect this number to change over time?

The number of vehicles registered in the UK annually is approximately 2 million post-pandemic, and close to or over 3 million pre-pandemic. The number of new registered vehicles was 2.2 million in 2021, so for this analysis we will assume that this volume will remain constant over the coming years. The total number of vehicles in the UK was 39.5 million, so we can also assume this will remain relatively constant over the coming decade, as it has been for the last five years, assuming that older vehicles remain as second hand vehicles, and every year the same number of vehicles come off the road as are added.

In 2021, 5% of all newly registered vehicles were plug-in hybrids and 10% were electric. This number is slowly but steadily increasing. In May 2022, for instance, electric vehicles were 12.4% and plug-ins 5.9%. We can project a relatively steady increase of this ratio before reaching 100% by 2030. There will still be non-EVs registered after 2030 as HGVs, for example, will not yet be electric, but in comparison to the total number of vehicles, we can use this as a good enough approximation.

These projections still mean that we need to wait until 2034/35 for over half of all UK vehicles to be electric. But there is cause for cautious optimism - we shouldn’t let the scale of the challenge deter efforts to develop and implement the strategies we need. This timeline suggests that there is sufficient time and need to develop strategies to support EV infrastructure deployment, consider future rollout of technologies within the sector and the changing role a local authority will play over the coming years.